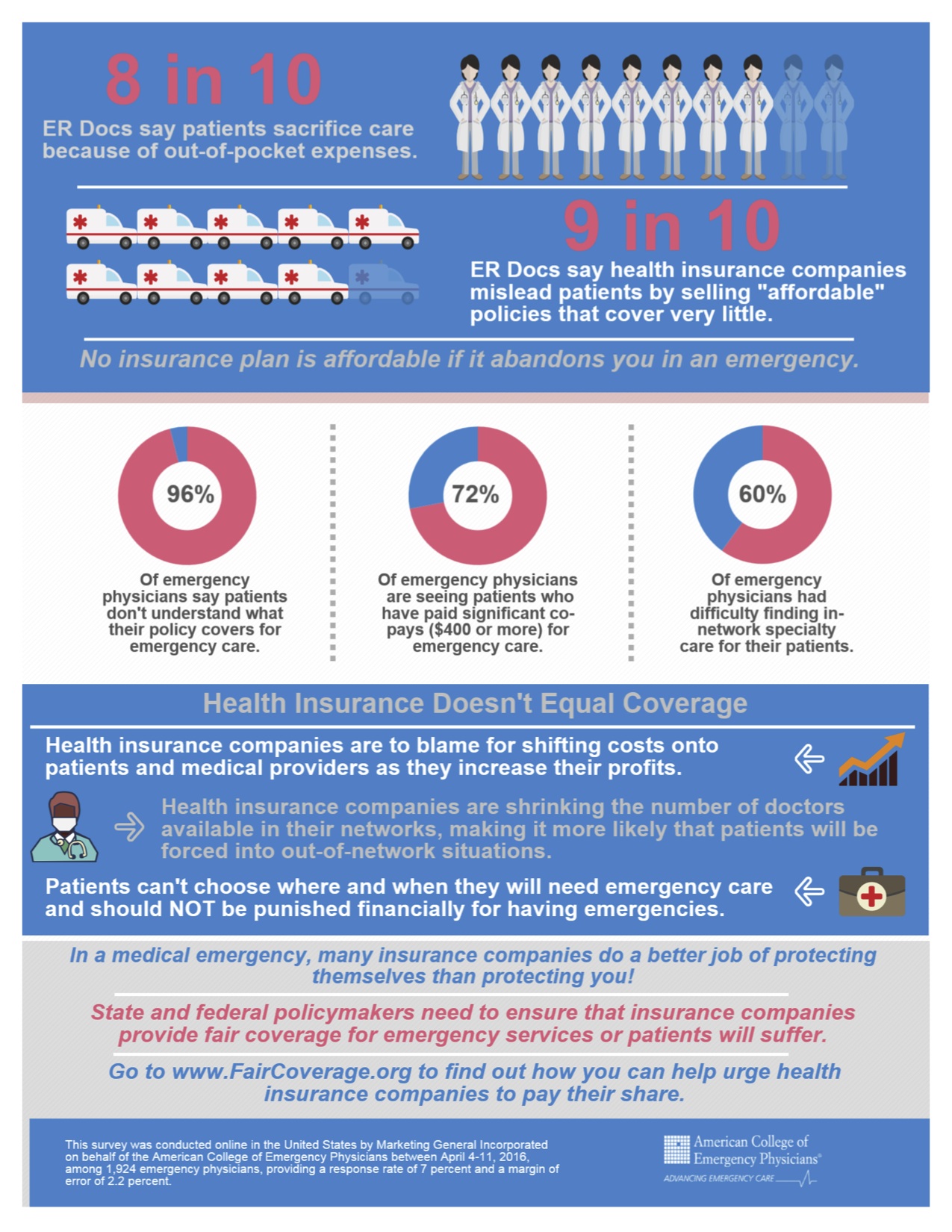

A whopping 96% of my colleagues reported in that their patients don't know what their health insurance policy covers for emergencies. Is it wishful thinking that they'll never have an emergency? Probably in part, but it's also likely due to clever marketing by the health insurance industry: insurance companies lure patients with low premiums that ultimately don't cover very much. As a physician, you may not think this is your problem but it is everyone's problem.

Each day, we are seeing patients who have significant copays of $400 or more for emergency care. It might as well be $4,000 for some people. That will surely deter some patients who may not need emergency care but it will also deter some patients who do. Eight in 10 emergency physicians are seeing patients who have sacrificed or delayed medical care because of concern for high out-of-pocket expenses, co-insurance or high deductibles. This is dangerous. A patient who has delayed necessary care comes to you sicker and with more complex needs than a patient whose problem was solved early. It elevates risk for both the patient and the provider.

Nobody chooses when they will need emergency care, and they should not be punished financially for having emergencies or discouraged from seeking medical attention when they are sick or injured. Significant copays and high deductibles effectively do exactly that.

Insurance companies are creating narrow networks of medical providers to increase profits, making it more likely that patients will be out of network. When plan reimbursements do not cover the cost of providing services, physicians must choose between billing patients for the difference and going unpaid for services. Or opting out of networks entirely, leaving patients fewer choices for care.

The insurance industry has a history of data manipulation. For example, a major health insurer for years fraudulently calculated and significantly underpaid doctors for out-of-network medical services. The company was successfully sued by the State of New York and they, along with other insurers, paid a $350 million settlement, of which $50 million was used to create the Fair Health database. This is the best mechanism available to ensure transparency and to make certain that insurance companies don't miscalculate payments. However, The Department of Health and Human Services recently handed a victory to the insurance industry by ruling that they can reimburse essentially whatever they like for emergency care. It is no secret that whatever they like is as close to nothing as possible.

Insurance companies must provide fair coverage for their beneficiaries and be transparent about how they calculate payments to physicians. They need to pay reasonable charges, rather than set arbitrary rates that don't even cover the costs of care. Insurance companies need to stop exploiting federal law -- -- in order to reduce coverage of emergency care, knowing emergency departments have a federal mandate to care for all patients, regardless of their ability to pay.

State and federal lawmakers need to ensure that health insurance plans provide adequate rosters of physicians and fair payment for emergency services. Emergency physicians are encouraging all patients to investigate what their health insurance policies cover and demand fair and reasonable coverage for emergency care. We also encourage all physicians to join in this fight – do it for you and do it for your patients.

, is president of the American College of Emergency Physicians. He is vice chair of emergency services for Ochsner Health System in New Orleans and assistant to the CMO in the areas of physician engagement and the patient experience. He is a graduate of Harvard College and Harvard Medical School.